It is perhaps the most underrated aspect of investing, but I’m telling you – liquidity matters!

It is so ubiquitous that we hardly pay any attention to it…we assume that for every seller there is a buyer, we assume that markets are efficient and that assets are always “fair value”, and we assume that we’ll be able to convert our assets into cash at a time that suits us, for a price that suits us… well think again.

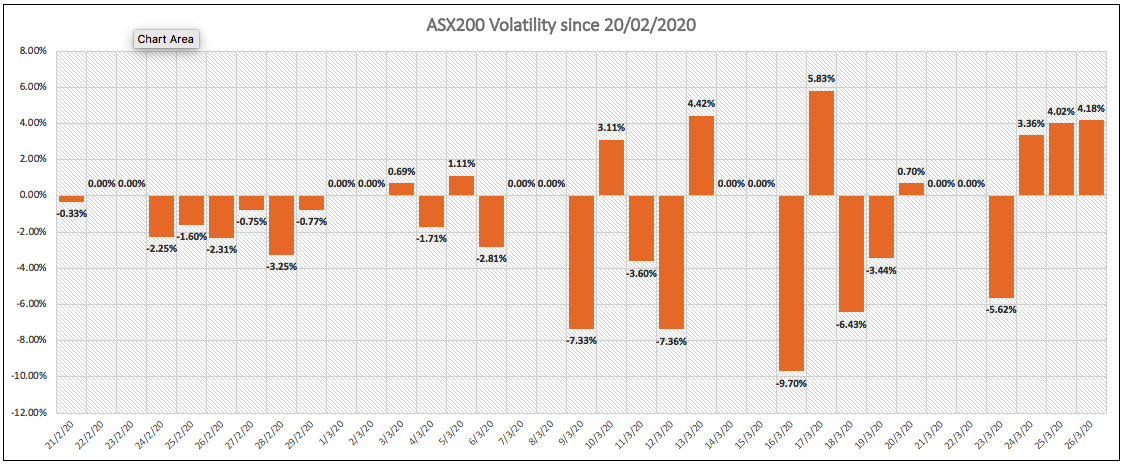

The last month has to be one of the most incredible months I have seen on the ASX. Daily record swings in either direction, wild emotional trading, and intraday moves of 12%+ for the entire index!

Through the crazy swings either way, larger downside moves resulted in the fastest 30% fall for both the ASX & the S&P500 in history bar the 1987 ‘Black Monday’ crash. Whilst there are plenty of underlying drivers there are largely two things responsible for such incredible drop, and when they meet… it’s ugly. *Those two things are fear & liquidity (or rather a lack thereof).

*That’s not to say there isn’t plenty of rational selling in there too.

Liquidity refers to the ability to turn an investment back into cash (or vice versa) efficiently, without causing major changes in the price of the asset. When sellers and buyers meet in an orderly market $360,000,000 of Commonwealth bank shares can change hands in a single day, and the share price might only move by 0.5%. But what happens when the buyers dry up and the sellers want to sell…like really want to sell? On the 9th of March, $530,000,000 of CBA shares were sold and because buyers were thin on the ground, the share price was pummelled a whopping -6.47%.

Now that is ugly by anyone’s standard, but we’re talking about one of (if not the most) liquid stocks on the Australian share market! Imagine for a second you’re holding an asset with essentially zero liquidity – something like I don’t know… a house, a half-built unit block, a major infrastructure project, a micro-cap stock, or shares in an unlisted business…. and then liquidity dries up. Its a big deal and you can suffer major falls in the value of your asset, and in some cases be completely unable to convert some or any of it into cash.

Don’t believe me? Well, Australias biggest super fund changed its mandate around 18 months ago to allow it to freeze its property option for up to 2-years in the event of ‘exceptional circumstances’. Australians love affair with property really is far more dangerous than most people realize.

To exacerbate the issues seen recently, illiquidity issues have started impacting credit markets and even safe-haven assets like US government bonds.

Why…?

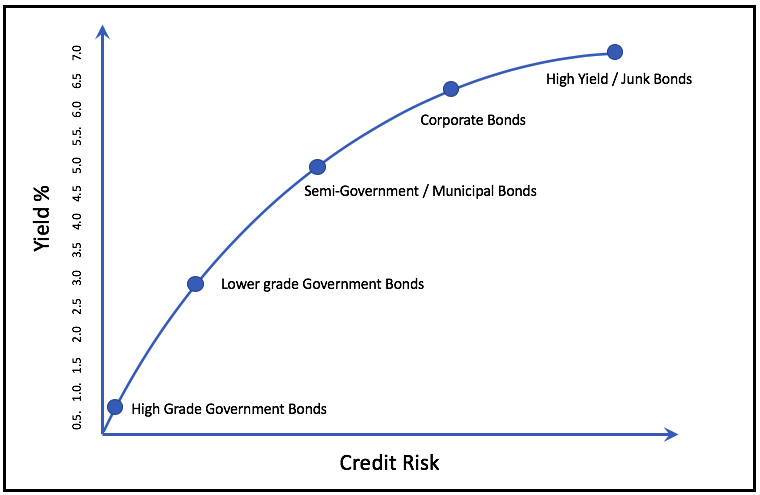

Government bonds (provided they’re issued by governments with strong credit ratings) usually act as defensive assets and rise in value (yield lower) when risk assets sell-off. However, such is the need for cash at the moment that sellers will sell anything & everything to get it. It’s not so much the credit risk that sovereign governments will default on their coupon repayments to investors. It’s that those coupon payments have gotten smaller and smaller (interest rates have fallen) and the number of sellers overwhelms the number of buyers.

Think about it…

- Fund managers & private investors who are overweight in higher-yielding (riskier) bonds due to the ‘hunt for yield’.

- Investors who are underweight cash & need it to meet expenses

- People cashing up to prepare to go into lockdown

- Pension & Super funds cashing up to meet redemptions from members who haven’t managed their own liquidity (insufficient savings buffers)

- Fund managers forced to sell (even good) assets to meet redemption requests.

- Redemptions on Index funds that sell underlying holdings indiscriminately – more on this in another post.

These illiquidity issues just get worst and worse the lower the credit rating of the issuer.

So, it pays to manage your liquidity!

Your cashflow & your balance sheet (or that of the companies you’re invested in) are absolutely critical, so pay attention to them… not just the P&L Statement!

Make sure you have enough access to cash & / or credit to get through rough periods and you’ll never be a forced seller. In fact, you’ll be in a wonderful position to scoop up high-quality assets that have been force-sold or thrown out with the bathwater.

So where else does the concept of liquidity rear its head?

- Typically the smaller the company, the less liquid its securities (shares), so volatility is far more extreme for small-cap and micro-cap stocks.

- Companies who have poor balance sheets and/or cashflow and have large share-price falls may need to raise capital from equity markets or credit markets – either way, the terms won’t be favourable! High interest on credit (due to the increased risk of the borrower), and enormous dilution for investors if new equity is issued at lower prices.

- Many Super funds invest in private equity & unlisted assets (such as direct property or infrastructure). The issue with ‘unlisted assets’ is they only get valued quarterly. Thus far for example, the fall in the value of these assets is not yet reflected in the reports & unit prices of the funds. So beware, if everything looks rosy on the surface for now, it might not be once these assets get re-valued.

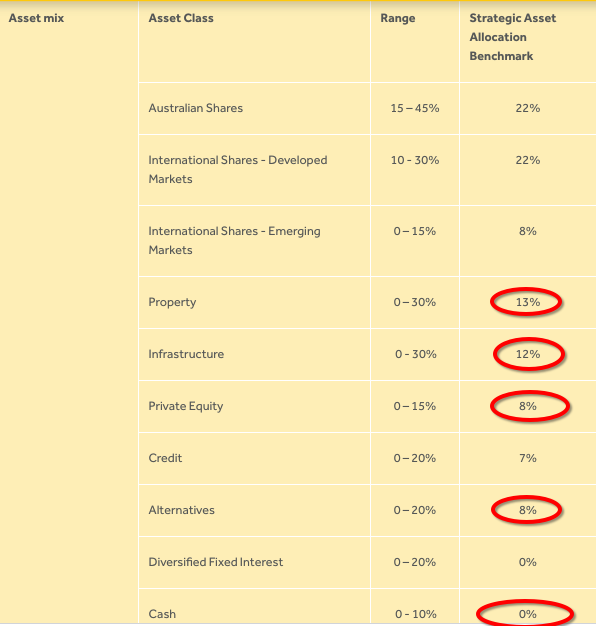

- Super funds and/or managed funds that have liquidity issues may freeze redemptions. Again, think property-related, micro-cap stocks, funds investing in private equity or esoteric assets, high yield mortgages etc etc. (Imagine thousands upon thousands of Australians wanting to access $10,000 of their super under the recently announced government relief measures. *Now imagine their fund is heavily invested in illiquid assets and doesn’t hold much cash.

*The fund I’ve just described is HOSTPLUS’ ‘balanced’ option, which rather than being ‘Balanced’ was invested in 93% growth assets at the time of APRA’s recent Super Fund Heatmap. Its target asset allocation is 0% cash, 33% in property & private equity, 8% in alternatives and 0% in liquid defensive assets like high-grade government bonds. HOSTPLUS is the default fund for Hospitality & Tourism workers – many of whom have just lost their jobs and may need to make redemptions. Where is the cash going to come from?

It’s one of the most underappreciated facets of investing, but liquidity matters! Stay safe, stay solvent, and make sure you’re in a position to capitalise on opportunities that arise from the mismanagement of liquidity.

Saul.